Where the Wyoming LLC Story Falls Apart

That "simple" limited liability company is rarely simple. It works on paper, but it often fails in real life. For non-U.S. founders, the perceived asset protection can become a direct path to personal tax liability. The Wyoming LLC tax mistakes that expose your personal assets begin the moment you prioritize the entity over your own residency. The structure you think is protecting you could be the very thing that makes you the target.

The Simple Wyoming LLC: The Hidden Risks

You followed the standard advice. Open a Wyoming LLC. It seems smart, efficient, and gives you a foothold in the U.S. It is the move everyone from online forums to business gurus recommends.

This advice is dangerously incomplete. It solves one problem while quietly creating a much larger one. The real risks are not in the Wyoming LLC formation documents; they are in what happens after.

Why “Open a Wyoming LLC” Is Repeated Advice

The advice is everywhere because it is easy. Wyoming law offers privacy protections, and the state has no income tax. The LLC registration process is streamlined and inexpensive.

These features are attractive. They create the illusion of a perfect, one-size-fits-all solution for non-US founders looking to establish a business entity. Promoters highlight the low costs and strong asset protection statutes, selling you on simplicity.

What they don't explain is that these benefits exist in a vacuum. They apply to the LLC name and entity itself but do not automatically shield you, the foreign owner, from your own country's tax authorities. It is a simple answer to a complex problem, and simple answers sell.

The Appeal of Stripe Atlas and Easy U.S. Business Setup

Platforms like Stripe Atlas have made U.S. business setup feel like a checklist. It is presented as a turnkey solution that provides instant access to the U.S. market.

The appeal is undeniable. You gain access to the U.S. business bank account system and payment processors, lending your business an air of legitimacy. The process is designed to be frictionless, handling key steps for you:

- Complete the LLC formation.

- Obtain an Employer Identification Number.

- Facilitate opening a business bank account.

This ease of use is a feature, not a strategy. These platforms solve the technical steps of creating a business entity. They do not solve for your personal tax residency.

Recognition vs Reality: What Non-U.S. Founders Miss

You get a U.S. legal entity. You have a business name and documents from the United States. You feel legitimate. This is the recognition you paid for.

The reality is different. Your home country’s tax authority does not care about your LLC's certificate from Wyoming. They care about where you live and where you make decisions. As the LLC owner, you are the controlling mind, and the income tax liability flows through the entity directly to you.

They don’t see a U.S. company. They see you, a resident of their country, earning income. The LLC becomes transparent, and the asset protection you thought you had disappears under their tax code.

Who Needs To Rethink Their Structure

This is not for U.S. residents. The rules for you are different. This is for the non-U.S. founder who thinks they have found a clever loophole by using a limited liability company.

It is for the entrepreneur running a global business through a U.S. entity, believing the structure provides a complete shield. Your business structure needs a second look if your primary goal was chasing perks instead of building a sound foundation for asset protection.

Non-U.S. Founders Running Global Revenue Through A Wyoming LLC

You live outside the United States. You serve clients globally. But all your revenue funnels through a Wyoming LLC, which you believe isolates your income in a low-tax US business structure.

This is a fundamental misunderstanding. The U.S. might view your LLC as a pass-through entity, but your home country views you as a tax resident. All that global income is attributable to you personally, and the LLC is just a conduit.

Your tax liability is not determined by your company's location but by your personal residency. Each tax year you operate this way, the exposure for foreign owners grows. You are not immune; you are the primary target.

Anyone Chasing Points, Stripe Access, and Visibility

The strategy was never about real asset protection. It was about perks. You wanted the U.S.-based credit card to earn points. You needed Stripe Atlas for a payment gateway. You wanted the visibility of a U.S. entity.

These are short-term optimizations. Business owners chase these benefits without understanding the cost. The legal documents from Wyoming give you a sense of security, but they don't alter the fundamental tax reality.

You traded long-term structural integrity for immediate convenience. This is a bad trade. The points you earn will not cover the bill for retroactive tax assessments.

The Steps Everyone Follows and Where They Go Wrong

The path is well-trodden. You choose a name, file the articles of organization, and draft an operating agreement. Each step feels official, like you are building a fortress and gives you a false sense of security.

The problem is not the steps themselves; they are technically correct. The problem is that they are incomplete. You are building a house with no foundation, and you will not realize it until the storm hits.

Forming the Entity: What Happens Behind The Scenes

You hire a registered agent. You pay the filing fee to the Wyoming Secretary of State. You receive your approved documents, creating a new business entity separate from yourself.

Behind the scenes, nothing has changed about who holds the power. You are still the one making decisions and profiting. For tax purposes, the IRS itself considers a single-member LLC owned by a non-resident a "disregarded entity."

This means they look past the entity and see the owner. If the IRS does this, you must assume your home country’s tax authority will do the same. The legal fiction of the entity provides no tax shield.

Opening U.S. Bank Accounts Without True Residency Planning

With your EIN, you approach U.S. financial institutions. Many online banks now cater to non-resident founders, so you do not even need a physical address in the U.S. Within a few business days, you have a bank account.

This feels like the final piece of the puzzle. You can now accept U.S. dollars and operate like a local company.

But this bank account is just a tool. It does not create "substance" in the U.S. It is an account owned by an entity that you, a non-resident, control. The money trail leads directly back to you.

Stripe Atlas Tax Problems: False Perceptions of Safety

Stripe Atlas simplifies the mechanics of formation. It even provides templates and guidance on tax forms, creating a powerful, false perception of safety. You assume that because a major company facilitated the process, it must be strategically sound.

Stripe Atlas is a formation service, not a tax advisor. It ensures your LLC is set up correctly for U.S. tax purposes as a legal entity. It does not account for your personal tax obligations in your home country.

The LLC taxation rules it helps you navigate are only one-half of the equation. The other half (the one that exposes you) is waiting back home.

Pass-Through Taxation: The Exposed Reality

The term "pass-through taxation" is often sold as a benefit, meaning no double tax in the U.S. For a non-resident founder, it is the mechanism of your exposure.

The profits do not stay in the LLC; they pass through to you, the owner. This makes you the taxable unit, not the company. Your income tax returns, filed in your country of residence, are where the liability truly lands.

How Control and Decision-Making Make You the Taxable Unit

.png)

Your LLC structure is just a shell. The critical question tax authorities ask is: Who controls it? As the sole LLC member, you are the "mind and management" of the business.

- You make all the decisions.

- You direct its activities and sign contracts.

- You manage its finances.

Because control resides with you in your home country, tax authorities argue that the business is effectively managed from there. The legal entity in Wyoming is irrelevant. The tax rate that applies is not Wyoming's zero percent but the rate in your country. They don’t see a U.S. company. They see you.

Why Foreign Tax Authorities Look Beyond the LLC

Tax treaties and anti-avoidance rules are designed for this exact scenario. Your home country's tax agency is not impressed by your Wyoming formation documents. They are trained to identify substance over form.

They see a resident of their country earning income and parking it in a foreign entity with no real economic connection to its location. This is a classic red flag. The LLC offers no asset protection from this kind of scrutiny.

They have the authority to disregard the US tax entity and assess tax directly on you, the foreign owner. Their own tax code is their only concern.

Double Taxation: Born From The Wrong Order

Double taxation is not a mistake you make on a form. It is a structural failure. It is born when you choose your entity before you have a coherent residency plan.

You create a mismatch between where your company legally exists and where you personally exist for tax purposes. This conflict is the source of your double tax liability, and it was baked in from day one.

The Residency vs Entity Mismatch

.png)

You have a Wyoming business entity. But you have a tax residency in France, Australia, or Brazil. These are two different legal and tax worlds.

The entity's location is a matter of public record. Your residency is a matter of fact, determined by where you live and work. When you channel income through an entity for tax purposes while being a resident of a high-tax country, you create a conflict.

Your home country will claim its right to tax your worldwide income. The U.S. may also claim a right to tax income connected to a U.S. business. You are now caught between two systems, all because you prioritized the entity over your residency for the tax year.

Retroactive Exposure: Compound Risk Over Time

The risk is not just for this tax year. It is retroactive. Tax authorities can look back several years, and each year you operate with this flawed structure, the potential tax liability compounds.

- Year 1: A small amount of unreported income.

- Year 2: The amount doubles, plus penalties.

- Year 3: The tax agency opens a formal audit.

What started as a simple LLC has become a multi-year financial problem. The asset protection you sought is gone. As the LLC owner, you are personally liable for the back taxes, interest, and penalties.

When A Wyoming LLC Doesn’t Protect Your Personal Asset

Limited liability is the core promise of an LLC. It separates your business debts from your personal assets. This works for commercial liabilities. If a customer sues your business, your personal assets are generally safe.

This protection does not extend to your own tax obligations. When your home country's tax authority determines you owe income tax, they are not suing your LLC. They are assessing you, the individual.

The LLC's liability shield is irrelevant. Your personal assets are fully on the table to satisfy that tax debt. You are the taxpayer, not the LLC.

Points, Miles, and The Perks Mirage

You focused on the small wins. The credit card points, the easy Stripe integration, the professional-looking U.S. address. These perks are tangible and immediate. They feel like smart business optimizations.

But they are a mirage. They distract from the foundational weakness of your structure. The LLC owners optimized for the trivial and ignored the critical.

Comparing Short-Term Benefits to Long-Term Liability

Let's be surgical. You gained a few thousand dollars in credit card rewards. You saved a few hours on payment gateway setup. These are the short-term benefits.

Now, weigh that against the long-term liability for business owners.

- Potential for years of back taxes at your home country's rate.

- Penalties and interest that can exceed the original tax obligations.

- Legal and accounting fees to defend yourself in an audit.

The comparison is not even close. The asset protection you sacrificed is worth infinitely more than the points you collected.

Stripe Atlas Optimization vs Real Structural Protection

Stripe Atlas provides an excellent service: it automates a process. It optimizes for speed and convenience in company formation. This is not the same as structural protection.

Real asset protection comes from a coherent strategy that aligns your business entities with your personal residency. It is deliberate, planned, and often slower. It requires thinking about tax liability, control, and substance.

A registered agent service and an EIN are just components. They are not a strategy. Relying on an automated formation platform for your international tax strategy is like using a calculator to perform surgery.

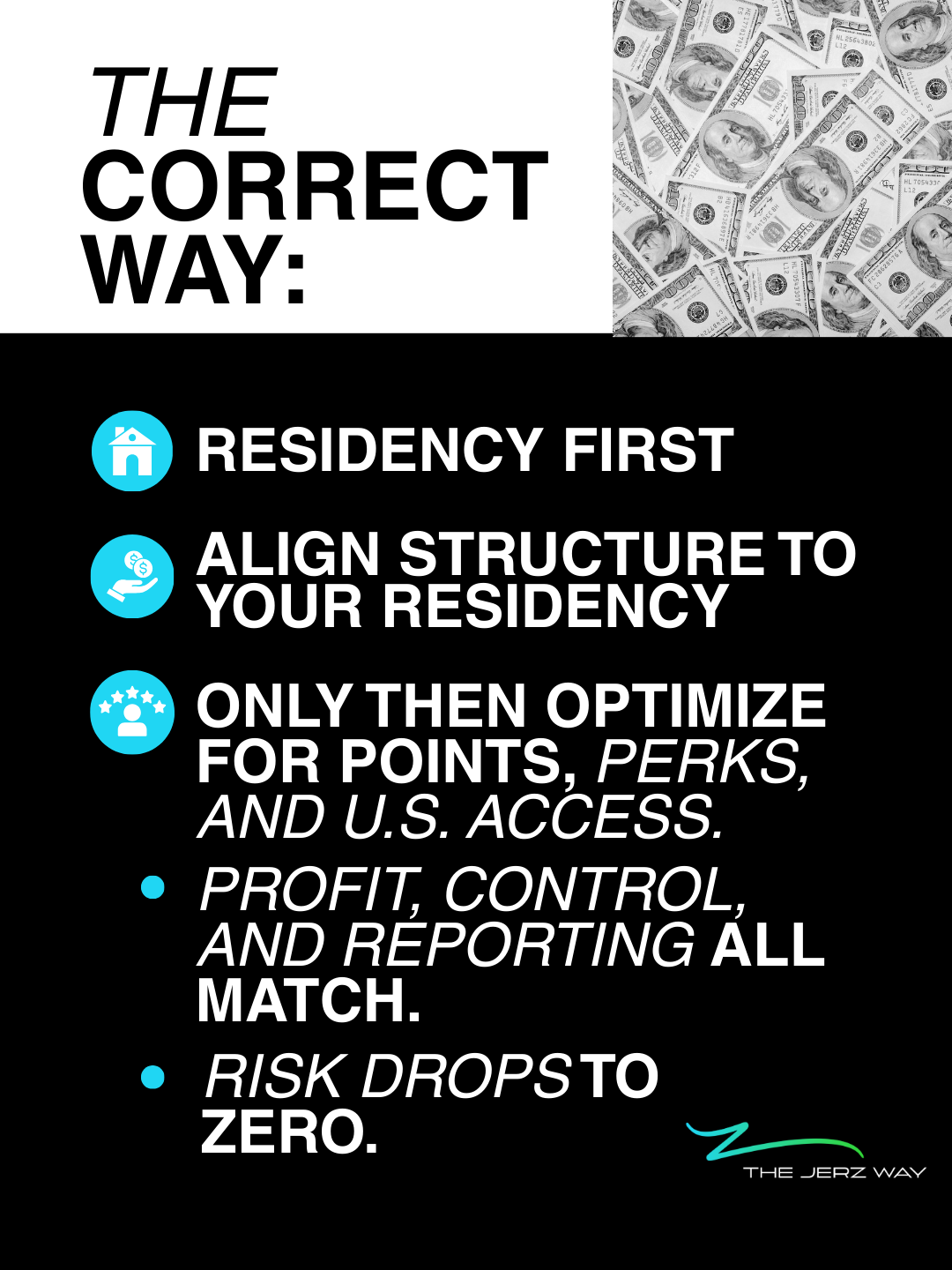

The Right Sequence: The Jerz Philosophy

The default advice gets the order wrong. It tells you to start with the entity: the "what." This is a path to exposure.

The correct approach starts with you: the "where." Your business structure must serve your residency, not the other way around. This is the only way to achieve real asset protection.

Why Residency Comes Before Structure

Your tax residency is the anchor of your financial world. It is the one fact you cannot easily change. It determines which country has the primary right to tax your income.

Therefore, any business structure must be built around this anchor. You must first understand the rules of your home jurisdiction. What is considered resident-controlled income? What are the anti-avoidance provisions?

Only after you have a clear picture of your residency-based obligations can you design an entity that complies with them. Starting with the entity before understanding your residency is like building a roof before you have walls.

Optimization Is Only Safe After Residency Alignment

Once your business structure is aligned with your residency, then you can optimize. You can look for efficiencies in tax treaties. You can choose entities that offer both liability protection and compliance with your home country's rules.

Optimization is the final step, not the first. When done in the correct order, it is safe and effective. When done first, it is reckless.

Hard Rules: How to Avoid Asset Exposure

There are no loopholes, only rules.

- Rule 1: Your personal tax residency dictates your primary tax obligations. This is non-negotiable.

- Rule 2: An entity in a zero-tax jurisdiction does not make your income tax-free.

- Rule 3: Control determines taxation. If you control the entity from your home country, the income is taxable there.

Following these rules protects your personal assets from tax authorities. Ignoring them exposes everything you own. Asset protection is not about finding a clever trick; it is about adhering to the fundamental rules of international tax after your LLC registration.

Follow The Jerz Way