The Traditional Retirement System Wasn’t Built for You

The traditional retirement system is presented as the cornerstone of a secure financial future. You are encouraged to contribute diligently to a 401(k) or IRA, entrusting your money to a system that promises stability decades from now. This article challenges that promise. We will explore how this system was not necessarily built for your benefit but to trap capital, limiting your access and control. It’s time to question the narrative and examine the hidden risks to your retirement income and financial goals.

You Were Told Retirement Was the Ultimate Goal

You were told to work hard, save diligently, and wait for age 65. This was the blueprint for a good life: decades of labor in exchange for a few golden years of freedom. You accepted this trade-off because it was presented as the only responsible path.

But what if the path itself is the problem? The issue isn't your discipline or your savings rate. The problem is the structure of the traditional retirement system itself, a system designed with interests other than your own in mind.

The Foundational Belief: Work Now, Live Later

The cultural narrative you’ve been sold is simple: postpone your life. Defer your dreams, your travel, and your passions until you reach full retirement age. This "work now, live later" mindset is deeply embedded in our society.

This belief system encourages you to trade your most valuable asset, your time, for a promise of future security. A financial advisor might map out a plan showing a large number on a screen, but that number is decades away and contingent on factors outside your control.

Common mistakes people make when planning for retirement often stem from this foundational belief. They focus solely on accumulating a nest egg for a distant future, ignoring the wealth they could be building and the life they could be living today. They sacrifice autonomy now for a permission-based future.

Why the Traditional Retirement System Feels Safe But Isn’t

.png)

The traditional retirement system creates an illusion of financial security. It feels safe because it’s institutionalized, endorsed by employers, and promoted by the financial industry. The steady contributions from your paycheck and a growing account balance provide a sense of progress.

However, this feeling of safety masks significant retirement planning flaws. Misconceptions about how this system operates can severely impact your financial future, leaving you vulnerable when you can least afford it.

Here are a few reasons why this perceived safety is a myth:

- Conditional Ownership: You don't truly control the money in these accounts.

- Guaranteed Erosion: Your savings are systematically devalued by inflation.

- Moving Goalposts: The rules governing taxes, withdrawals, and access can and do change.

Deferring Life: How This Narrative Serves Institutions Over Individuals

So, who truly benefits from the "work now, live later" model? Consider the vast pools of capital held in retirement accounts. This money is managed by financial institutions that generate fees from your locked-in savings for decades.

The system is designed to accumulate and hold capital, providing a predictable stream of revenue for asset managers and a stable source of funding for markets. Your personal financial future is secondary to the stability and profitability of the system itself.

This is one of the most pervasive myths about retirement planning. While you defer your life, your capital is put to work for others. You trade control and liquidity for a tax benefit you may never fully realize, all while your purchasing power quietly erodes.

The Deferred Life Plan: Retirement Myths Exposed

Deferring your life is not a savings strategy; it's a life-delay mechanism. The traditional retirement system is built on a series of myths that encourage this delay, convincing you to trade present-day freedom for a future that is far from guaranteed.

Let's begin to dismantle these myths. We will look closer at who really controls your time, the psychological toll of this deferred plan, and why the fundamental flaws in this system often go unnoticed for years.

Permission-Based Futures: Who Controls Your Time?

When your wealth is locked in a traditional retirement account, you are living in a permission-based future. You need permission to access your own money before a certain age, and you face penalties if you do. Your timeline is not your own; it's dictated by the rules of the plan.

This is a critical distinction between retirement planning and retirement income planning. The former focuses on accumulation within a rigid structure, while the latter should focus on creating accessible sources of income you control. The traditional system forces you into the first category.

You are not building a future on your own terms. You are building a future that requires you to ask for an allowance from your own savings, tethered to a system that prioritizes its rules over your life's needs and opportunities.

Pattern of Delayed Fulfillment and Its Psychological Costs

.png)

Constantly postponing gratification creates a pattern of delayed fulfillment that carries significant psychological costs. You spend your healthiest, most energetic years working for a future that may never arrive in the way you envision. This can lead to a sense of unfulfillment and regret.

This approach conditions you to devalue your present time. It becomes a resource to be endured rather than enjoyed. Your financial goals become disconnected from your life goals.

The psychological costs are substantial and often overlooked by a financial advisor focused on numbers:

- Chronic Anxiety: Constant worry about whether you're "saving enough" for a distant, unknown future.

- Loss of Optionality: Inability to pursue new opportunities, start a business, or take a sabbatical because your capital is inaccessible.

- Diminished Health: The stress of a deferred life can take a toll on your physical and mental health long before you reach retirement.

Why Retirement Planning Flaws Go Unnoticed for Decades

The flaws within the traditional retirement system are subtle and designed to remain hidden over long time horizons. The market goes up, your statement balance grows, and you feel like you're on the right track. This nominal growth masks the underlying issues.

Because the consequences of these flaws, like the true impact of inflation or future tax law changes, won't be felt for 20, 30, or 40 years, there is no immediate feedback loop. You're driving a car with a slow leak in the tires, and you won't notice until you're stranded on the side of the road.

Financial planners themselves are often trained within this very system, and they may not recognize these structural flaws. They help clients optimize within the existing rules, not question the rules themselves. This perpetuates the cycle, and the flaws go unnoticed until it's too late to change course.

The “Tax Advantage” Mirage of 401(k)s and IRAs

.jpeg)

The primary hook for 401(k)s and IRAs is the "tax advantage." You contribute pre-tax money, lowering your current income tax bill, and let it grow "tax-deferred." This sounds like a clear benefit, but it's more of a mirage.

This tax deferral is not tax reduction. You are simply kicking the tax can down the road to a point in time when tax rates are completely unknown. You are trading a known tax liability today for an unknown, and potentially much higher, one in the future.

401k Retirement Risks and IRA Tax Disadvantages Explained

The main drawbacks of using a 401(k) or an IRA are rooted in their structure. With a 401(k), your investment options are often limited to a small menu of funds chosen by your employer. Both accounts expose your savings to market fluctuations without giving you the liquidity to react strategically.

The IRA tax disadvantages are significant. You are essentially entering into a partnership with the government on your own savings, where they can change the terms of the deal at any time. Your future regular income is subject to future tax policy.

A benefit you can’t control isn’t a benefit. It’s a leash.

Changing Rules and Forced Distributions: A Moving Target

.png)

The rules of the game can change at any time. Tax laws are not static. Congress can, and does, alter the regulations surrounding retirement accounts, including contribution limits, withdrawal rules, and tax treatment. You are making a 40-year plan based on today's rules, which is an incredibly risky bet.

Furthermore, the system forces your hand with required minimum distributions (RMDs). Once you reach a certain age, you are legally obligated to start withdrawing money from your traditional retirement accounts, whether you need it or not.

These forced withdrawals can push you into a higher tax bracket and accelerate the depletion of your savings. You lose the ability to manage your tax liability strategically. Your financial decisions are dictated by compliance, not by your personal needs or market conditions.

Illusion of Control: Why Retirement Accounts Don’t Truly Benefit You

You might have a login to view your account and a limited menu of investment choices, but this creates an illusion of control. Real control is the ability to access your capital when you need it, for whatever reason you choose. Traditional retirement accounts fail this test.

Even the company match, often touted as "free money," is part of the trap. It incentivizes you to lock up your capital in a restrictive system. It's a golden handcuff that keeps you tied to an employer and a savings vehicle that limits your financial freedom.

Poor retirement planning that relies solely on these accounts sacrifices true agency for perceived simplicity. It impacts your chances of financial freedom by systematically stripping you of liquidity, control, and the ability to adapt to life's opportunities and challenges before your official retirement date.

Inflation: The Silent Threat to Retirement Savings

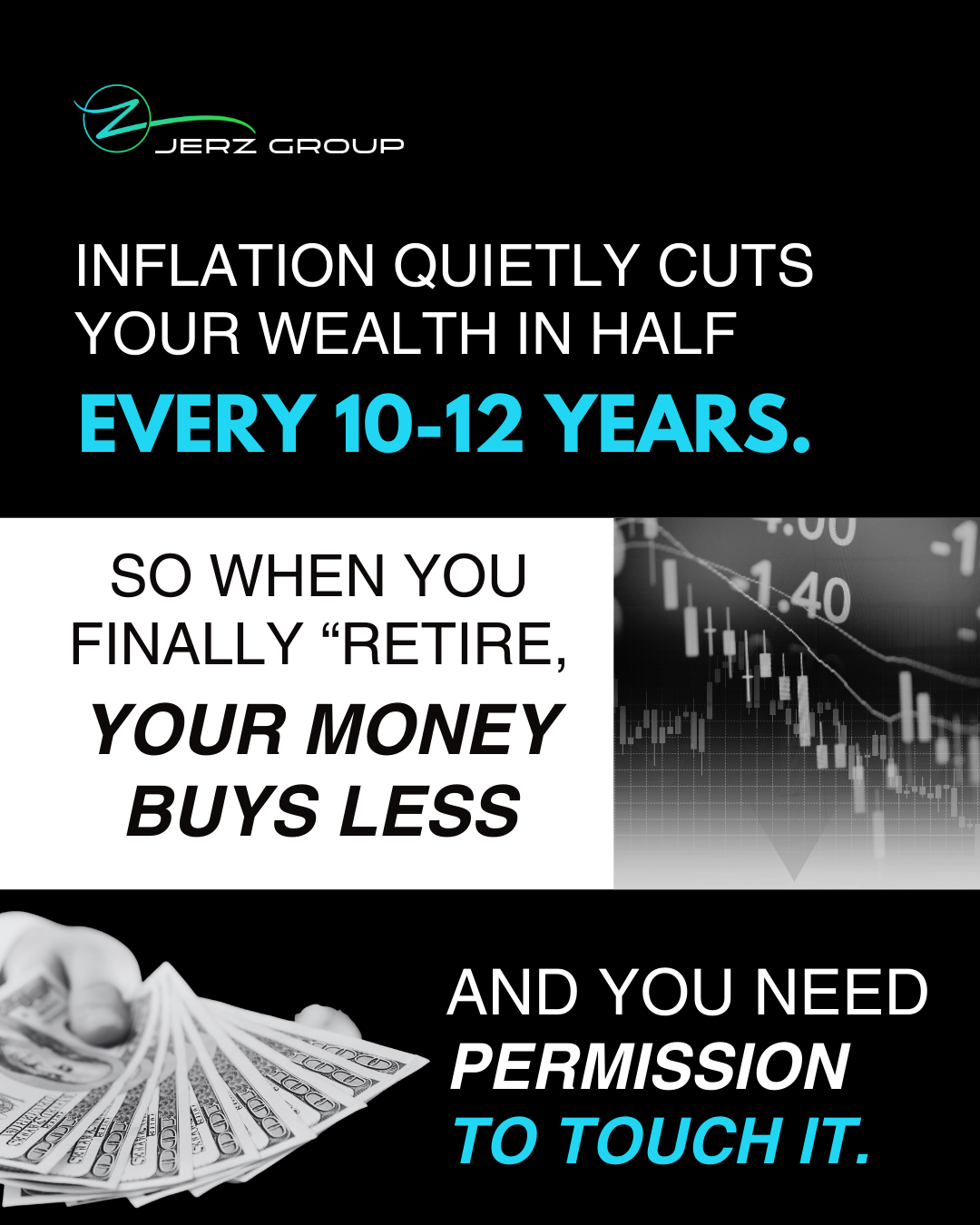

Beyond taxes and control, there is a quieter, more corrosive threat to your retirement savings: inflation. Over the decades you are saving, the purchasing power of your money is constantly being eroded. The dollar you save today will not buy a dollar's worth of goods tomorrow.

This isn't a minor detail; it is a fundamental flaw in any long-term savings plan that doesn't actively account for it. Your retirement income might look large in nominal terms, but its real-world value could be shockingly low.

Why Retirement Plans Fail in an Inflationary Environment

Traditional retirement planning often uses simple calculators that project future growth but fail to adequately model the corrosive effect of long-term inflation. A plan that targets a $2 million nest egg in 30 years might completely ignore that $2 million will have the purchasing power of less than half of that in today's money.

Your financial goals become a moving target. As the cost of living, health care, and other essentials rises, the adequacy of your savings account diminishes. You are saving for a finish line that is constantly being pushed further away.

One of the most critical habits to avoid common retirement planning flaws is to stop thinking in nominal dollars. You must think in terms of future purchasing power. If your plan doesn't, it's already on a path to failure.

Nominal Growth vs. Real Wealth: The Misleading Numbers

It’s easy to be lulled into a false sense of security by watching your account balance go up. This is nominal growth, the increase in the number of dollars you have. Real wealth, however, is about what those dollars can actually buy.

The difference is critical. You can experience positive nominal growth while your real wealth declines. Your statement shows you're getting richer, but your ability to afford your desired lifestyle is shrinking.

Consider the following:

- Nominal Growth: Your account grows from $100,000 to $107,000 in a year (a 7% return).

- Real Wealth: If inflation was 4% that year, your actual purchasing power only grew by 3%. If your investments returned only 3%, your real wealth was stagnant, despite your statement showing a gain.

- The Trap: Focusing on the 7% gain makes you feel successful, while the silent 4% loss goes unnoticed.

Inflation as Policy, Not Accident: What It Means for Your Savings

.png)

It is crucial to understand that a moderate level of inflation is not an accident or a sign of a broken economy. It is an intentional policy tool used by central banks and governments. A consistent, low level of inflation encourages spending and investment and helps manage government debt.

What this means for your savings account is that the system is designed to devalue your idle cash over time. Your long-term savings are sitting in the direct path of this policy.

This isn't a conspiracy; it's just economics. But failing to recognize this means you are fundamentally misunderstanding the environment in which you are trying to build wealth. You cannot win a game when you don't know all the rules, and intentional inflation is a key rule of the financial system.

Locked and Conditional: Do You Really Own Your Retirement?

This brings us to the central question: do you really own the money in your retirement account? If ownership means the right to access, use, and control your property, then the answer is no. Your retirement savings are not truly yours.

They are conditionally assigned to you, available only under a specific set of rules and circumstances dictated by the government and your plan administrator. This is the definition of being rich on paper but poor in reality, with a high net worth you cannot freely use.

The Impact of Withdrawal Penalties and Restricted Access

Withdrawal penalties are the bars on your financial cage. The 10% penalty for accessing your money before age 59½ is a powerful deterrent that prevents you from using your own capital for immediate opportunities or emergencies.

This restricted access has profound impacts. A brilliant business idea, a chance to invest in real estate, or the need to cover unexpected health care expenses cannot be funded with your retirement savings without incurring a significant penalty.

You are forced to seek other, often more expensive, forms of capitafdel like personal loans, while your largest asset sits untouchable. This lack of liquidity is a massive, hidden cost of the traditional retirement system.

Compliance Risks: Age Restrictions and Law Changes

Your retirement account is subject to significant compliance risks. The age restrictions are clear, but the tax laws surrounding these accounts are constantly in flux. What is a Roth IRA today might have different rules in a decade.

A financial advisor might help you navigate the current tax laws, but no one can predict what they will be when you reach your retirement date. You are anchoring your entire financial future to a legislative environment that is guaranteed to change.

This creates a state of permanent uncertainty. You are not in control; you are a passenger in a vehicle driven by politicians and policymakers, hoping they don't change your destination mid-journey.

True Ownership: Access, Timing, and Control Compared to Locked Accounts

.png)

True ownership is defined by three elements: access, timing, and control. Locked retirement accounts fail on all three fronts. You lack access without penalty, you cannot control the timing of your withdrawals in later life, and your decisions are governed by external rules.

Contrast this with assets you truly own. These are assets that provide flexibility and allow you to build wealth on your own terms.

Consider these examples of true ownership:

- A Profitable Business: Generates cash flow now and is an asset you can sell or pass on.

- Cash-Flowing Real Estate: Provides regular income and appreciates in value, with capital you can access via loans.

- A Brokerage Account: Offers daily liquidity, allowing you to buy or sell assets based on your strategy and needs, not age-based rules.

Modern Wealth Structuring: How the Wealthy Build Freedom

The wealthy don't build financial freedom by relying on the traditional retirement system. Instead, they focus on structure, control, and cash flow. Their approach is not about picking a better mix of stocks for their 401(k); it's about building a financial fortress outside of it.

This isn't about secret loopholes or complicated schemes. It's a fundamental shift in mindset from accumulation for the future to building accessible, resilient wealth today. They prioritize systems that give them optionality and control over their assets.

Asset Separation and Jurisdictional Awareness

A core principle of modern wealth structuring is asset separation. This means not holding all your assets in one basket, under one set of rules, or in one legal jurisdiction. The wealthy use legal structures like trusts and LLCs to protect their assets from creditors and legal threats.

Jurisdictional awareness is also key. They understand that where an asset is held can be as important as what the asset is. Some jurisdictions offer more favorable tax laws or stronger asset protection, and they strategically place assets to take advantage of these benefits.

This is not something a typical financial planner will discuss. It requires a more sophisticated understanding of legal and financial systems, moving beyond simple investment products to focus on the underlying structure of your wealth.

Liquidity, Optionality, and Cash Flow Over Tradition

While the traditional system emphasizes locking money away, modern wealth strategies prioritize liquidity, optionality, and cash flow. Liquidity is having access to cash or assets that can be quickly converted to cash. It is the power to act when opportunity arises or crisis strikes.

Optionality is the direct result of liquidity. It is the freedom to choose your path, to invest, to pivot, to wait, to stop working without asking for permission. It's the opposite of being trapped by withdrawal penalties and age restrictions.

Ultimately, the goal is to create sources of income and cash flow now, not just a pile of money for later. This provides true financial freedom vs retirement, allowing you to design your life today instead of endlessly preparing for a future you can't control.

Follow Jerz